The 7 Cognitive Biases That Cost You Thousands

These mental traps are normal—and expensive. This guide shows you how to recognize and avoid them before choosing a mortgage.

Anchoring: Why the first rate you see distorts all future comparisons

Present Bias: How focusing on monthly payment costs you $30K+ over time

Choice Overload: When too many options lead to paralysis or bad decisions

Loss Aversion: Why you fear losing money more than gaining it—and how lenders exploit this

Status Quo Bias: The hidden cost of defaulting to your bank

Sunk Cost Fallacy: When to walk away from a pre-approval you invested time in

Recency Bias: How yesterday's rate move shouldn't drive today's decision

Get Your Free Guide

By submitting this form, you acknowledge that you have read, understood, and agree to be bound by the SMS Policy and Terms.

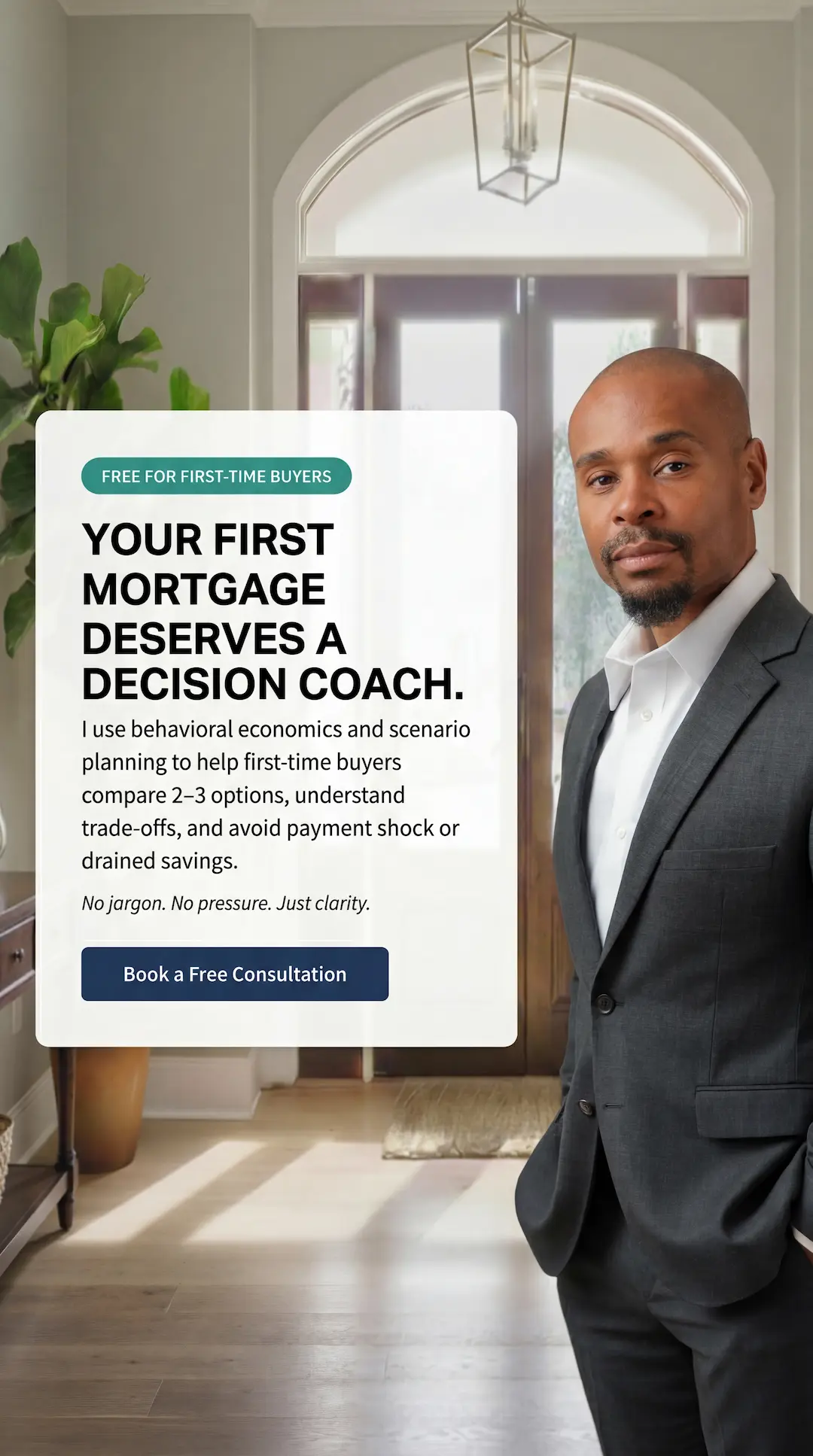

The mortgage market is noisy. Your decision doesn't have to be.

Rates, points, terms, programs—there's a lot to consider. But for first-time buyers, only four decisions actually matter:

Payment Comfort

Can you sleep at night with this monthly cost?

Total Cost Over Time

What do you actually pay over 1, 5, or 10 years?

Cash Flexibility

Are you preserving enough emergency savings?

Future Optionality

Can you refinance if rates drop, or move if life changes?

Decision Coaching vs. The Traditional Approach

The difference isn't the rate. It's whether you actually understood what you were signing.

The Traditional Approach

- Pushes one "best rate" option

- Commission-driven recommendations

- Focuses on closing the deal fast

- Limited scenario comparison

- You hope you chose right

Decision Coaching — Mo Phanor

- Presents 2–3 structured scenarios with real trade-offs

- Uses behavioral economics to remove bias

- Focuses on YOUR financial goals and comfort

- Framework-driven, not product-driven

- You KNOW you chose right

What are you optimizing for?

The "best" mortgage isn't a product type—it's the one that aligns with your goals. Start here.

Lowest Monthly Payment

For buyers who want budget breathing room. Typically involves a 30-year fixed, lower down payment options, and avoiding points to preserve cash flow.

Trade-offs: higher total interest paid, slower equity build, possible PMI longer.

Lowest Total Cost

For buyers who can handle a higher payment to minimize lifetime interest. Typically involves 15–20-year terms, 20%+ down, and possibly paying points.

Trade-offs: higher monthly payment, more cash needed upfront.

Maximum Flexibility

For buyers who may move, refinance, or pay off early. Typically involves a 30-year term with prepayment ability or an ARM if confident in a 5–7-year timeline.

Trade-offs: may not have the lowest rate, rate risk if ARM.

Cash Preservation

For buyers who need to keep emergency savings robust. Typically involves 3–5% down, seller concessions or lender credits, and accepting a slightly higher rate to preserve cash.

Trade-offs: PMI costs, higher monthly payment, less initial equity.

Not sure which matters most? That's exactly what the Decision Checkup is for.

Book a Free Consultation